Daily Globe British Values, Global Perspective

Daily Globe British Values, Global Perspective

Related Articles

Raw materials prices are rising. Why? Will this continue?

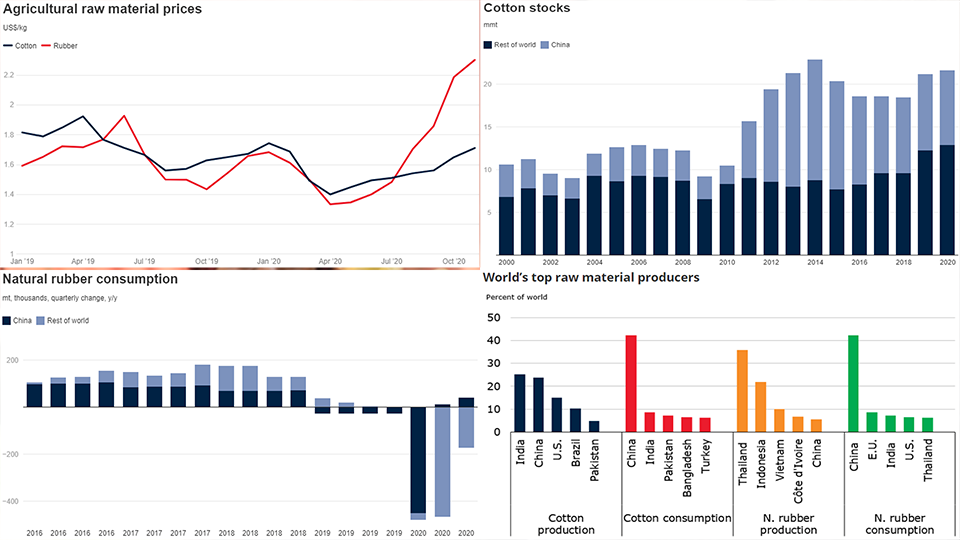

Cotton and natural rubber prices have experienced a sharp rise:

|

|

| World Bank Blog |

Notice that China is the main consumer.

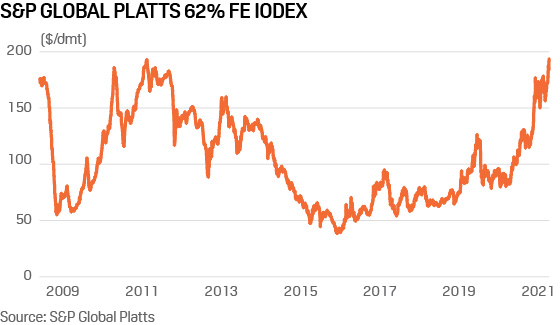

Iron ore prices are high:

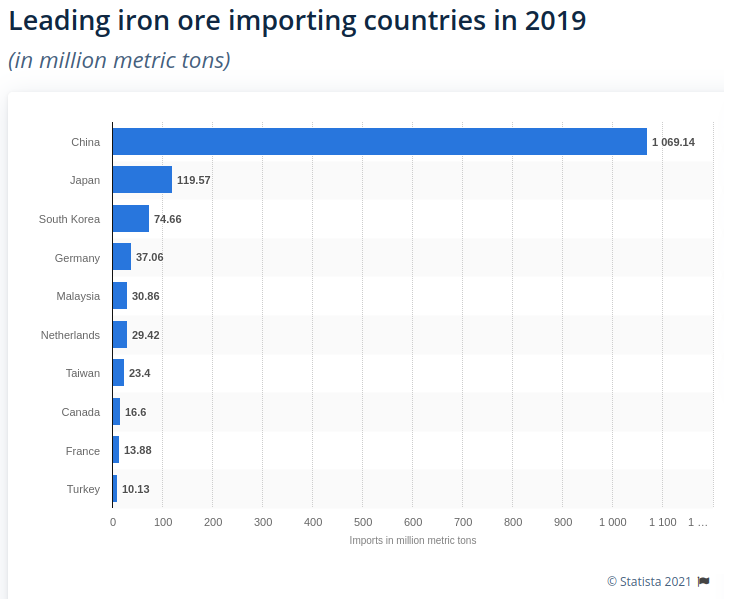

And China is the main importer:

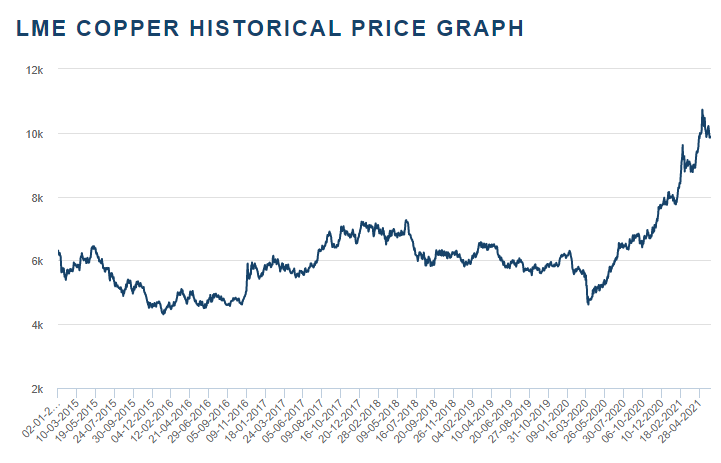

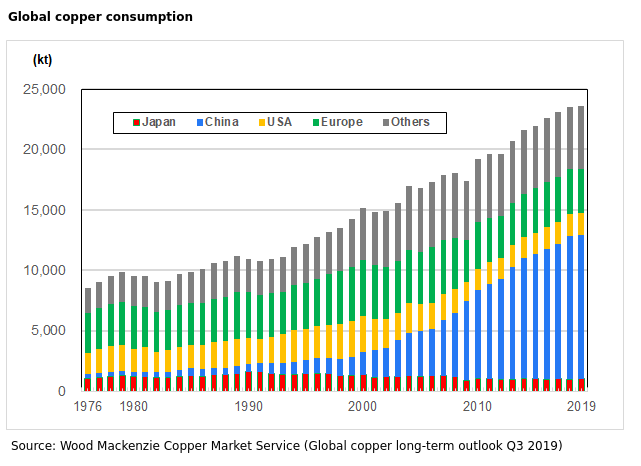

Copper prices are up:

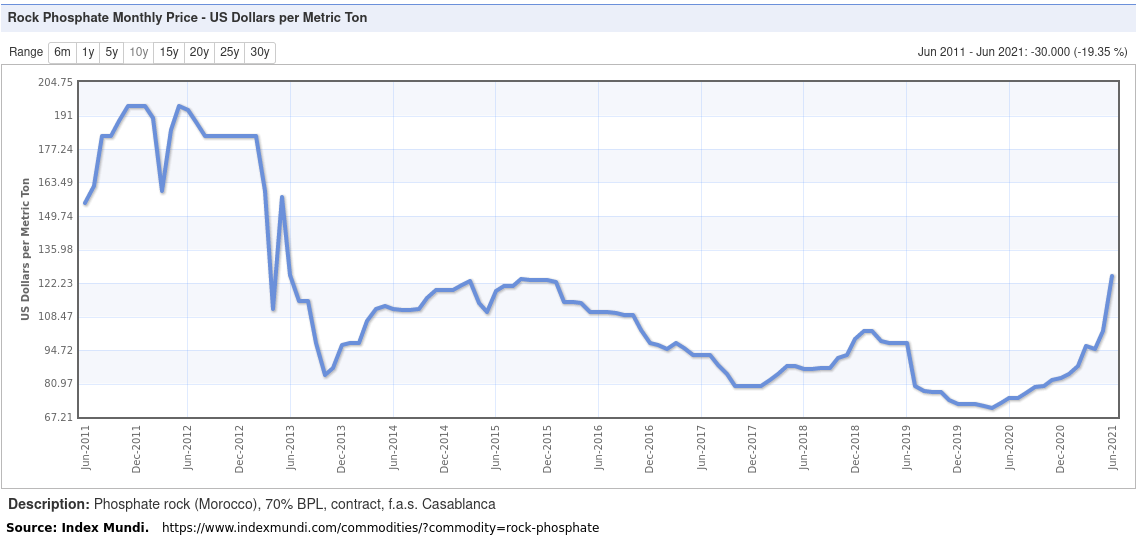

The failure of the price of copper production to keep pace with consumption is due to shortages of copper ore. It is not just copper reserves that appear too small to satisfy China. Phosphorus, an essential ingredient of agricultural fertilisers, is in short supply and has doubled in price over the past year.

|

| Index Mundi |

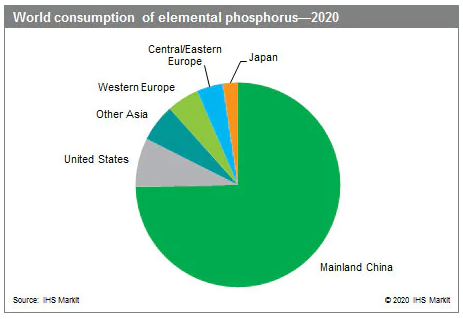

It will be no surprise to discover who is consuming the phosphorus:

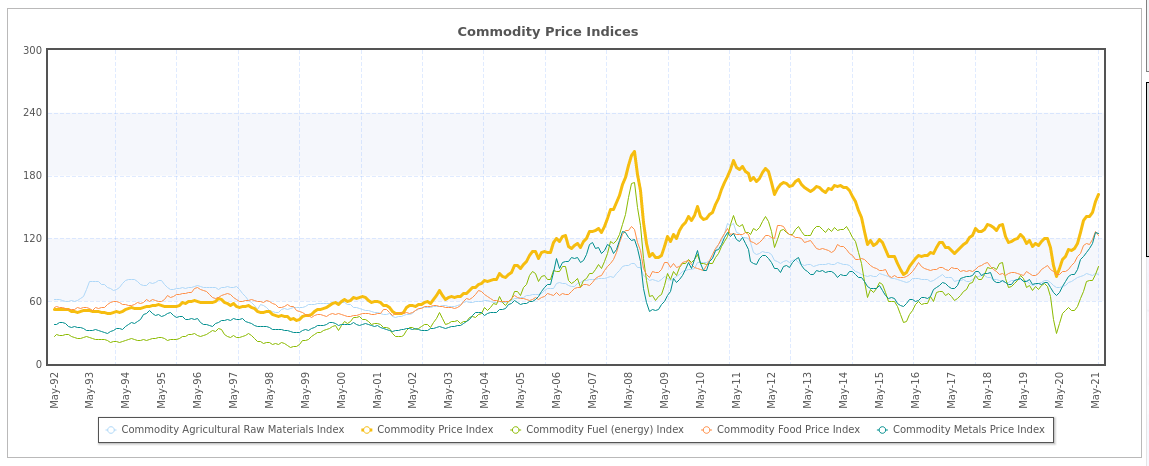

The pattern is the same over most commodities.

|

| Index Mundi |

Commodity prices are now highly unstable and their rise is due to demand from China.

Notice that everything except agricultural products has risen steeply over the past year. This rise in raw materials prices has a knock on effect on inflation. The Producer Price Index for the UK has been affected:

This has undoubtedly made a small contribution to the 2.5% June CPI figure for the UK. The USA has also experienced a jump in inflation. At present the effect is not serious and inflation is certainly more COVID related than PPI related but over the next decade raw materials prices, and more importantly access to raw materials, may become a major problem.

Notice that China is not just a major user of raw materials, it entirely dominates global raw materials demand. The recent increases in raw materials prices have largely been due to the demand from China.

China has only just begun its journey to true first world status. Although China has the largest economy in the world in Purchase Price Parity (PPP) terms each Chinese citizen has a per capita income of about $17000 PPP dollars whereas Western countries have a per capita income of about $50,000 PPP dollars. There is an unstoppable, pent up demand in China for at least doubling the size of the Chinese economy.

Western raw materials and military strategists and planners should pause for a moment to let the implications of China’s total dominance of global markets sink in. It is probably already the case that China can tell producers how to behave on most things except price.

The other global behemoth is India. India has almost the same population as China although at present India is 20 years behind China in industrial development. The recent border confrontations with China will be prompting the Indians to see economic development as an absolute priority.

Is there enough copper in the world to supply both India and China and the green energy market? There is probably a maximum of around a billion tons of exploitable copper in the ground and, with a likely average demand of about 30m tons pa or more for mined copper, the reserves will be severely depleted in about 30 years (see Peak Copper). Of course, copper will not actually run out, either copper will become too expensive or the price will become incredibly variable as substitutes are brought onto the market. Intense price variability will probably occur ten or fifteen years before copper becomes too expensive and too unpredictable to be part of reliably priced manufactured products. My guess is that in 30 years copper will be too expensive for use in mass produced goods and that there will be no good substitute for copper.

Copper is critical to the global economy. Off world mining will be big business in the future. *Invest in SpaceX now. However, expect a bumpy ride for commodity prices over the next 30 years.

*It seems like science fiction but if SpaceX achieves its aims we would expect much of metal processing to occur on Mars. Metals can almost literally be dropped from Mars to Earth but gravity means that only the most expensive finished goods will be transported in the opposite direction. If it can be established then Mars Colony will become dominant in the solar system.

This post was originally published by the author on his personal blog: https://pol-check.blogspot.com/2021/07/raw-materials-price-hikes.html